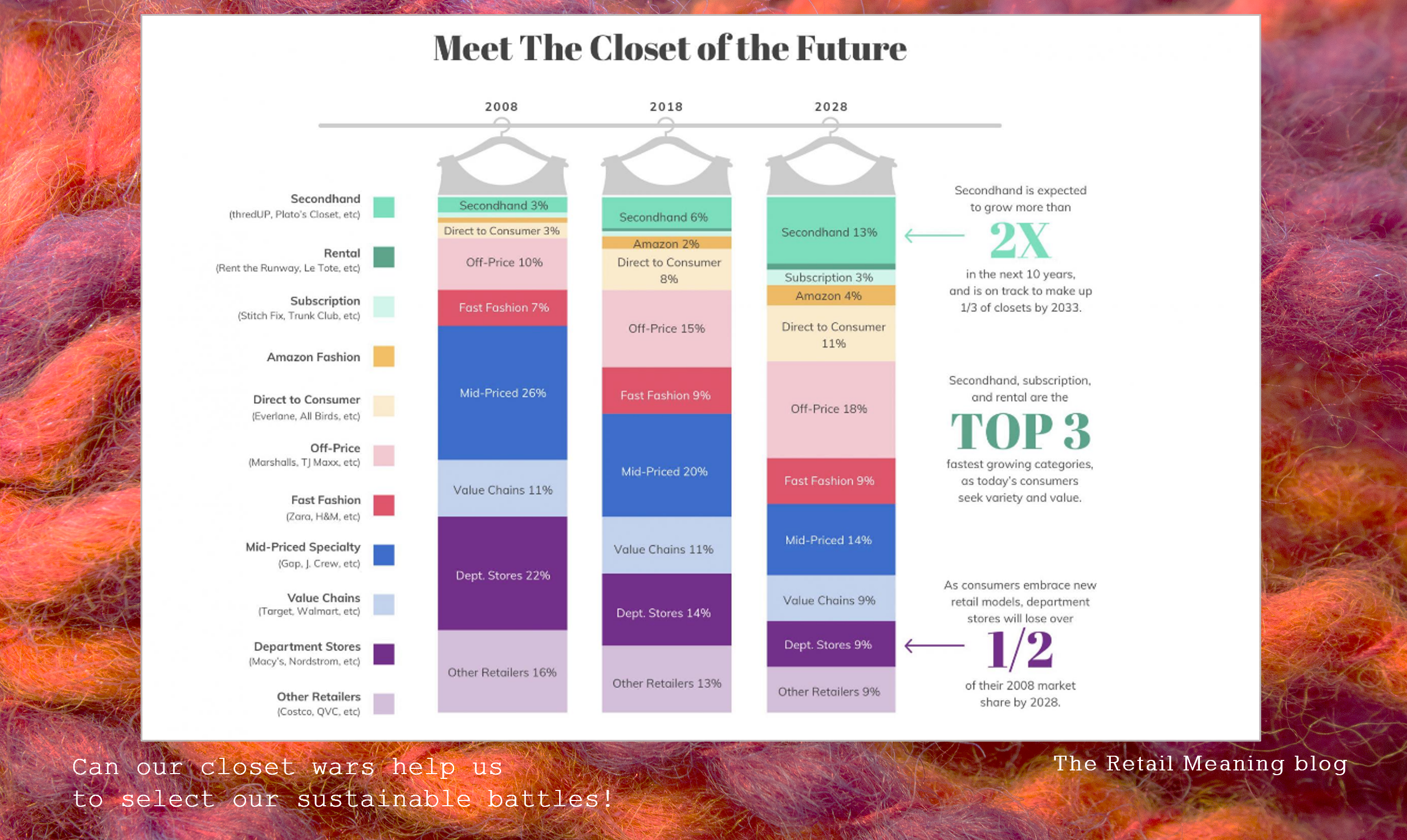

I love this chart! It was produced using Globaldata research and is now more than 5 years old. It predicted what types of retailer our fashion wardrobe would be bought from, up to the year 2028.

As we stand here in 2025 we can now see how accurate the predications were. Even if we consider this chart is for US closets, and the starting points different from the UK and elsewhere, the overall trends seem to have been very well anticipated.

The headline grabbers were that we would own more re-sell garments than we would fast-fashion. A rise in wardrobe space over 10 years of over 13% of these sustainable essentials.

And that the fast-fashion share would be largely static around 9%, as born out by the rapid rise and fall of names such as Missguided & Boohoo, in this very fickle market. Despite being identified as a very harmful sector environmentally, fast fashion remains irritatingly unmoved, but is not growing as a share.

The losers were predicted to be department stores and mid-price brands which has been born out with the collapse of Debenhams, House of Fraser and benchmarks such as GAP and J Crew retreating back to the US to save themselves.

Accurately predicted, has been the rapidly growing Direct-to-customer brands (DTC.) Everyone from mega sports brands to a myriad of more niche and ethical businesses were predicted to take up almost 15% of our space. This may in fact be higher today, as digital retailing has unleashed the visibility and customer loyalty of such brands.

What I particularly like about this study is that we are predicting & measuring the customers activities and preferences. This is not about market shares, revenues & profits of big business.

This predicts demand, market demand. And demand is particularly critical in the battle to create a sustainable fashion industry. Because the customer demand for greener businesses producing and selling less but better products is at the heart of creating change.

Where are the most important sustainability battles to be won? And who should we be battling against to suppress demand and slow the supply? Where should our energies be directed, on brands, on retailers, regulators & customers?

One huge question is whether we spend too much energy and angst on the fast-fashion market. On the one hand its product volumes are a disaster for the environment, however its market share is smaller than many think, its protagonists see no reasons to change, whilst its customers will also be some of the most difficult to change. Do we attack the supply with regulations and tariffs to stop the trafficking? Is this a better solution that using facts and figures in an attempt to quell the voracious demand for low-priced fashion?

Even though the traditional middle market is declining it still forms the largest individual group alongside established and emerging brands going DTM – predicted to be more than 25%.

None of these operators can win on price. They need to add ‘worth’ and value to their brands and products. Essentially they need to make more money from selling less, by monitorising ‘the extended life of each product’ and ‘the lifetime of each customer.’

Both the customers and the businesses in this sector would seem to be more of an open-door to change. The customer has an appetite for quality, and brand value. The messages and mechanisms of sustainability sit well with them.

Should it be a priority to leverage more resources into this area to change the demand model, and force the hand of suppliers to the greener industry their customers want? Should the weapons of choice be customer education, and practical and financial support to brands that are eager to learn new sustainable tricks.

A part of the market that is very successful and growing is ‘Off-price’ with TK Maxx at the head of the pack. The market share amounts to nearly a fifth of our wardrobes.

On the one hand their strategy has been to take excess stock (potentially heading for landfill) and to find a customer home for it. On the other they continue to increase the appetite of customers for volume over value. More dangerously they enable them to have both ‘value & volume.’

Is the sustainable battle here to be won through further encouragement and investment in the second-hand market? This growing market share includes side-hustlers, independent traders, brands striving to keep second-hand in-house, and a highly professional and increasingly coordinated charity sector. Should we all just buy from charities rather than big business?

In fact, should we only celebrate when the market share of both off-price and second-hand decreases to be a smaller part of a much smaller total market? Only then will we have won the battle against willful industry over-production in the search for profit through buying margins.

The battles are many and often complex, with the distinction between allies and foes increasingly blurred.

There are such extraordinary people doing amazing work across every area of sustainability, from new materials R&D, regenerative growing, recycling processes, circular models, product passports, transparent supply chains, re-sell, repair, rental, customer education and sustainable community building.

Every action is vital. But in any war, it’s always worth considering which are the most crucial battles to be won, who are our enemies, what strategies and weapons do we need to employ against them, and how we need to be coordinated.